- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Westinghouse Air Brake Technologies (NYSE:WAB) Completes US$1 Billion Share Buyback; Q1 Earnings Rise

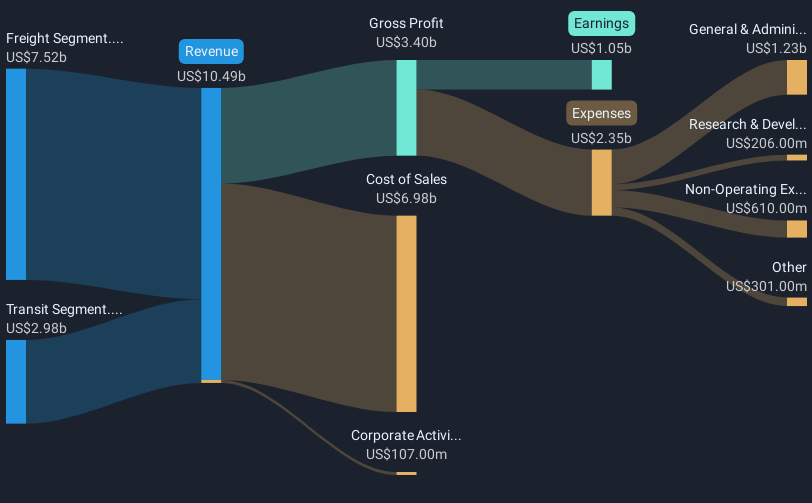

Westinghouse Air Brake Technologies (NYSE:WAB) recently reported promising first-quarter results, posting increased revenue and net income, along with an active share repurchase program, which likely contributed to a 7% price increase over the past week. These results reflect positively against the broader market conditions, where indices benefited from strong earnings reports and tariff optimism, with the market climbing by 2.3%. While Westinghouse's gains outpaced the general market, they are in line with a broader trend of renewed investor sentiment following robust quarterly performances across various sectors. Overall, the company's performance bolstered investor confidence amid a buoyant market week.

We've spotted 1 warning sign for Westinghouse Air Brake Technologies you should be aware of.

The recent 7% surge in Westinghouse Air Brake Technologies' share price, following its impressive first-quarter results, aligns with a broader industry pattern of positive investor sentiment and reaction to strong quarterly performances. This price change has brought the stock closer to the consensus price target of US$210.82, indicating a potential further upside from the current share price of US$171.76. The company's robust financial results and active share repurchase program could enhance revenue and earnings forecasts, leveraging global demand for locomotives and digital technologies.

Over a five-year period, Westinghouse Air Brake Technologies has delivered a total shareholder return of 217%, significantly benefiting investors with both capital appreciation and dividends. This exceptional long-term performance reflects the company's strategic positioning in the global market. When comparing the recent annual performance, Westinghouse exceeded both the US Market's 3.6% return and the US Machinery industry's -9.9% return over the past year, showcasing its resilience and market competitiveness despite economic uncertainties.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com