- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

3 No-Brainer Warren Buffett Stocks to Buy Right Now

In uncertain markets, it pays to follow proven wisdom -- and few investors have a track record as legendary as Warren Buffett. Since taking over Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B) in 1965, Buffett has weathered every market storm and consistently outperformed market benchmarks. Thanks to regulatory filings, investors get a quarterly look inside Berkshire's huge portfolio -- a rare window into the strategy of one of history's most successful investors.

With that in mind, three of Berkshire's largest holdings stand out as smart buys today.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

1. American Express

American Express (NYSE: AXP) is a favorite Buffett stock, and Berkshire hasn't sold a single share since it completed its $1.3 billion investment in 1995 for roughly 10% of the financial services company.

Today, the stock trades at about $250 per share, down 15% in 2025, and pays a quarterly dividend of $0.82 per share, representing an annual yield of 1.3%. Although the company doesn't raise its dividend yearly, it has a long history of increases, including four consecutive years of growth.

The company is also in the middle of a 120 million share repurchase plan, which was announced in March 2023, and has already lowered its share count from 744 million to 701 million, or roughly 5.6%. As a result of decades of stock buybacks, Berkshire's stake has soared to 21.6% without buying a single share since 1995.

Beyond its dividend and share repurchases, American Express delivered record revenue in 2024, up 10% year over year to $65.9 billion. With that revenue, the company -- which operates as a closed-loop network by issuing cards, extending credit to card users, and holding the loans on its books -- generated $10.1 billion in net income, a year-over-year increase of 21%.

As for risks, in a closed-loop network, American Express is susceptible to defaults, which are on the rise. To account for expected unrecoverable losses, it records non-cash provisions for credit losses. In 2024, provisions totaled $5.2 billion with a net write-off rate of 2%, up from $4.9 billion and 1.8% in 2023.

Today, American Express shares trade at a price-to-earnings (P/E) ratio of about 18, which aligns with its five-year median, suggesting that it's fairly valued.

AXP Shares Outstanding data by YCharts

2. DaVita

Berkshire Hathaway owns a 44% stake in the second stock on this list, DaVita (NYSE: DVA), a healthcare company that has recently shifted from solely a dialysis provider to offering more comprehensive kidney care services. It currently serves about 281,000 patients. DaVita's stock trades for about $140 per share in 2025, down about 6% for the year and about 22% below its all-time high. The drop can be attributed to a recent ransomware attack, which has affected some of its operations.

In 2024, the company achieved record financial results, generating $12.8 billion in revenue and $2.1 billion in operating income, representing year-over-year growth of 5.6% and 30.4%, respectively.

Despite its strong performance, DaVita faces some pressure on the balance sheet. The company holds $8.6 billion in net debt, compared to its $11.2 billion market capitalization. Still, with its free cash flow of $1.2 billion in 2024, management could pay it down if it chooses. Instead, management is aggressively buying back its stock, lowering its shares outstanding by 34% during the past five years, suggesting it believes the company is undervalued, as it trades at a price-to-free-cash-flow ratio of 7.9.

In the long term, DaVita's next growth phase will likely hinge on expanding its global footprint. As of the end of 2024, 84% of its 3,166 outpatient centers were based in the U.S. The company is actively pursuing international opportunities, recently expanding into Colombia and awaiting regulatory approval for a pending deal in Brazil, expected by midyear.

DVA Shares Outstanding data by YCharts

3. Kroger

Berkshire Hathaway has built up a nearly 8% position in Kroger (NYSE: KR) since its first purchase in 2019. The leading operator of grocery stores in the U.S. is a prominent dividend-paying stock, having paid and raised its dividend for 19 consecutive years. It currently offers a quarterly dividend of $0.32 per share, translating to an annual yield of about 1.8%.

While Kroger isn't known for high revenue growth, it remains a steady performer. In 2024, total sales reached $147.1 billion, up 1.8% from 2023, excluding special pharmacy sales, fuel, and an extra 53rd week. More notably, the company improved its profitability, posting $3.8 billion in operating profit -- a 31% increase from the prior year, again adjusting for the 53rd week.

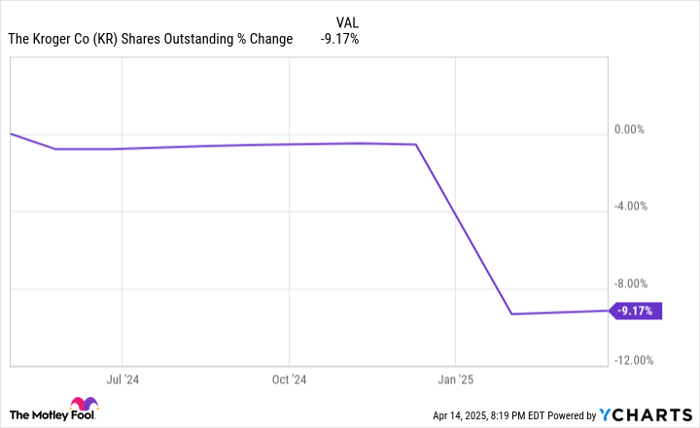

What really stands out, however, is Kroger's aggressive buyback activity. During the past year, the company has repurchased 9% of its shares outstanding. This move was primarily fueled by the collapse of its proposed acquisition of Albertsons Companies, which the Federal Trade Commission opposed.

With that deal off the table, Kroger redirected its capital to shareholders. In December 2024, management launched an accelerated $5 billion share repurchase program, with another $2.5 billion earmarked for buybacks once that is complete.

Regarding valuation, Kroger shares trade at 19.4 times trailing earnings -- above their three-year median of 16.1 -- indicating a potential premium. Still, for long-term investors, Kroger represents a stable, market-dominant grocery chain focused on returning capital to shareholders through dividends and stock buybacks.

KR Shares Outstanding data by YCharts

Are these Buffett stocks worth buying?

These stocks are not only key holdings in Berkshire Hathaway's portfolio -- they also share another important trait: each company is aggressively buying back its shares. As Buffett once explained, "The math isn't complicated: When the share count goes down, your interest in our many businesses goes up. Every small bit helps if repurchases are made at value-accretive prices."

For long-term investors looking to own market leaders and prioritize returning capital to shareholders, these Buffett-backed companies are worthy additions to your portfolio.

American Express is an advertising partner of Motley Fool Money. Collin Brantmeyer has positions in American Express and Berkshire Hathaway. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool recommends Kroger. The Motley Fool has a disclosure policy.