- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

What You Can Learn From MediWound Ltd.'s (NASDAQ:MDWD) P/S

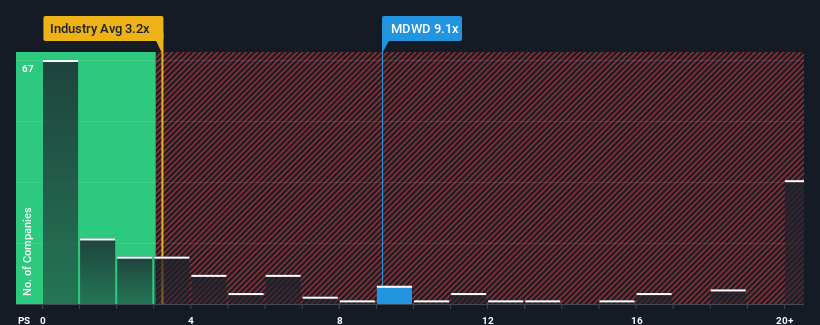

With a price-to-sales (or "P/S") ratio of 9.1x MediWound Ltd. (NASDAQ:MDWD) may be sending very bearish signals at the moment, given that almost half of all the Pharmaceuticals companies in the United States have P/S ratios under 3.2x and even P/S lower than 1x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for MediWound

How MediWound Has Been Performing

MediWound could be doing better as it's been growing revenue less than most other companies lately. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think MediWound's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like MediWound's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 8.2%. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 15% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 26% per year as estimated by the five analysts watching the company. That's shaping up to be materially higher than the 20% per annum growth forecast for the broader industry.

In light of this, it's understandable that MediWound's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On MediWound's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of MediWound's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with MediWound, and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on MediWound, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.