- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

The 3 Biggest Reasons Why This High-Yield Bank Is Better Than Citigroup

Citigroup (NYSE: C) is a bank you've likely heard of, given its long history and size. It is currently offering dividend investors a 3.5% forward dividend yield versus the 2.6% average for banks. That sounds attractive, but there's a history here. And you can get a roughly 5% yield from this giant industry peer that has been a more reliable dividend stock over time. Here's what you need to know.

The problem with Citigroup

The big problem with Citigroup is what happened during the Great Recession. That was a very difficult period for financial markets and for companies that were involved in mortgage lending. There was a very real concern that the world's financial markets were on the brink of collapse.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Citigroup ended up taking a government bailout and cutting its dividend. The dividend was slashed from $3.20 per share per quarter all the way down to a mere penny a share. That's a payment meant only to ensure that institutional investors can still own the stock (some institutional investors, like pension funds, mandate that they can only buy shares of companies that pay dividends). The share price got crushed along the way.

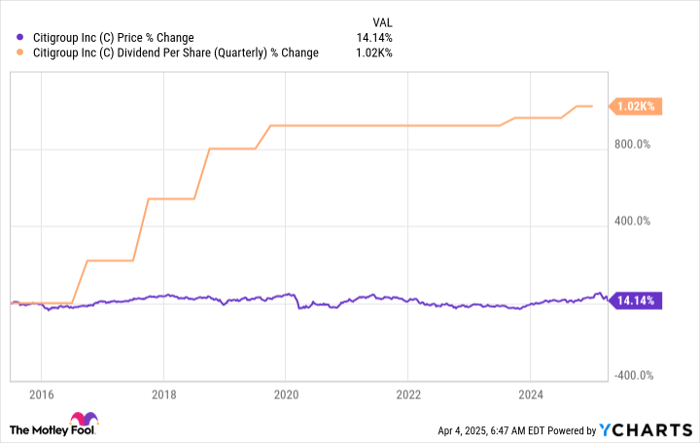

That was a long time ago, and Citigroup's business has notably recovered from that hit. The bank's dividend has increased over 1,000% during the past decade (admittedly, from a very, very low base). However, the stock has only risen by about 15% or so. This hasn't been a great investment in a lot of ways.

Investors should go with TD Bank instead

A better choice has been and will likely continue to be Canadian banking giant Toronto-Dominion Bank (NYSE: TD), which is more commonly called TD Bank. Canada's banking regulations are very strict, which has left its largest banks with entrenched market positions and a conservative ethos that pervades all aspects of their operations. TD Bank didn't have to cut its dividend during the Great Recession.

The impact of that difference has been huge for dividend investors. As the chart above highlights, neither Citigroup's stock price nor dividend have fully recovered from the Great Recession hit. That event looks like a small blip on TD Bank's chart lines. (Note that TD Bank's dividend is paid in Canadian dollars, so the amount U.S. investors receive fluctuates along with exchange rates.)

TD Bank's conservative and more consistent business and more reliable dividend are the first two big reasons it will likely be a better option than Citigroup for most investors. But then there's its lofty 5% or so dividend yield. That's way more than you'll get from Citigroup, which should probably raise an eyebrow.

TD Bank's U.S. operations were used to launder money. That resulted in a large fine, costs to upgrade its money laundering controls, and an asset cap. The asset cap only applies its U.S. operations, but this division was expected to be the company's growth engine. So, TD Bank is likely to grow only slowly in the years ahead until it assuages the concerns of U.S. regulators. It's not a good situation, but given the business foundation the bank has in Canada, it also isn't the end of the world.

Essentially, you are being paid a way above-average yield, and an above-Citigroup yield, to stick around and wait for TD Bank to get its U.S. business back on track. That's not a terrible thing if you are an income investor or if you like turnarounds. On the turnaround front, TD Bank is one of the lowest-risk turnarounds you are likely to see.

Citigroup is OK, but TD Bank is better

Investors probably wouldn't be making a huge mistake if they bought Citigroup. The company is in much better shape today than it was during the Great Recession. But you can do better with TD Bank. A more reliable business, a more reliable dividend, and a higher dividend yield add up to a much larger long-term investment opportunity.

Citigroup is an advertising partner of Motley Fool Money. Reuben Gregg Brewer has positions in Toronto-Dominion Bank. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.