- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Vishay Intertechnology, Inc.'s (NYSE:VSH) 41% Dip In Price Shows Sentiment Is Matching Revenues

The Vishay Intertechnology, Inc. (NYSE:VSH) share price has fared very poorly over the last month, falling by a substantial 41%. For any long-term shareholders, the last month ends a year to forget by locking in a 53% share price decline.

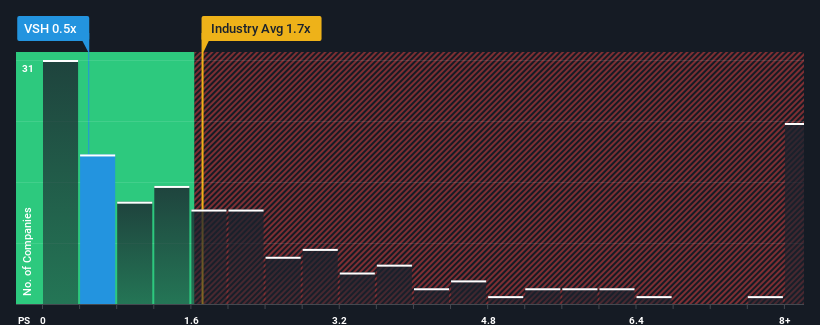

Since its price has dipped substantially, Vishay Intertechnology's price-to-sales (or "P/S") ratio of 0.5x might make it look like a buy right now compared to the Electronic industry in the United States, where around half of the companies have P/S ratios above 1.7x and even P/S above 4x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Vishay Intertechnology

How Has Vishay Intertechnology Performed Recently?

While the industry has experienced revenue growth lately, Vishay Intertechnology's revenue has gone into reverse gear, which is not great. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Keen to find out how analysts think Vishay Intertechnology's future stacks up against the industry? In that case, our free report is a great place to start .Is There Any Revenue Growth Forecasted For Vishay Intertechnology?

Vishay Intertechnology's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 14%. As a result, revenue from three years ago have also fallen 9.3% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 3.5% as estimated by the three analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 11%, which is noticeably more attractive.

With this information, we can see why Vishay Intertechnology is trading at a P/S lower than the industry. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Vishay Intertechnology's P/S

Vishay Intertechnology's P/S has taken a dip along with its share price. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As expected, our analysis of Vishay Intertechnology's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Vishay Intertechnology that you need to be mindful of.

If these risks are making you reconsider your opinion on Vishay Intertechnology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.