- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Benign Growth For Polaris Inc. (NYSE:PII) Underpins Stock's 26% Plummet

Unfortunately for some shareholders, the Polaris Inc. (NYSE:PII) share price has dived 26% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 64% share price decline.

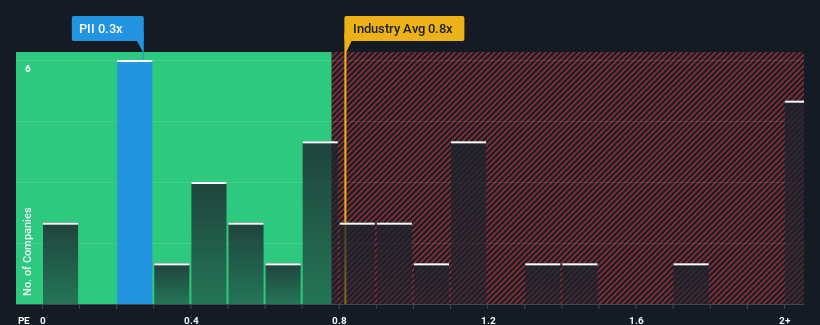

Even after such a large drop in price, given about half the companies operating in the United States' Leisure industry have price-to-sales ratios (or "P/S") above 0.8x, you may still consider Polaris as an attractive investment with its 0.3x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Polaris

How Polaris Has Been Performing

Recent times haven't been great for Polaris as its revenue has been falling quicker than most other companies. It seems that many are expecting the dismal revenue performance to persist, which has repressed the P/S. You'd much rather the company improve its revenue performance if you still believe in the business. Or at the very least, you'd be hoping the revenue slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Polaris will help you uncover what's on the horizon.Is There Any Revenue Growth Forecasted For Polaris?

In order to justify its P/S ratio, Polaris would need to produce sluggish growth that's trailing the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, revenue from three years ago have also fallen 2.9% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 1.2% per annum over the next three years. That's shaping up to be materially lower than the 3.4% per annum growth forecast for the broader industry.

In light of this, it's understandable that Polaris' P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Polaris' P/S?

Polaris' recently weak share price has pulled its P/S back below other Leisure companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Polaris' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

Plus, you should also learn about these 3 warning signs we've spotted with Polaris (including 2 which are potentially serious).

If you're unsure about the strength of Polaris' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.