- COTATIONS EN DIRECT

- APPRENDRE

- AIDE

WALL STREET JOURNAL

WALL STREET JOURNALFR

What UTS Marketing Solutions Holdings Limited's (HKG:6113) 85% Share Price Gain Is Not Telling You

UTS Marketing Solutions Holdings Limited (HKG:6113) shares have continued their recent momentum with a 85% gain in the last month alone. The annual gain comes to 136% following the latest surge, making investors sit up and take notice.

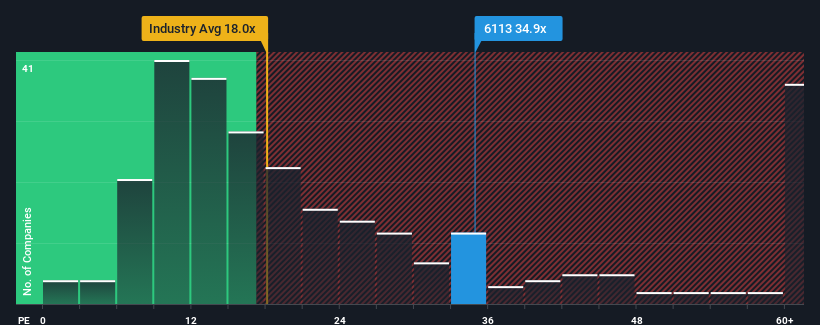

Since its price has surged higher, given close to half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") below 10x, you may consider UTS Marketing Solutions Holdings as a stock to avoid entirely with its 34.9x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times have been quite advantageous for UTS Marketing Solutions Holdings as its earnings have been rising very briskly. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for UTS Marketing Solutions Holdings

How Is UTS Marketing Solutions Holdings' Growth Trending?

In order to justify its P/E ratio, UTS Marketing Solutions Holdings would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 383% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 29% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 20% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that UTS Marketing Solutions Holdings is trading at a P/E higher than the market. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Key Takeaway

UTS Marketing Solutions Holdings' P/E is flying high just like its stock has during the last month. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of UTS Marketing Solutions Holdings revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Plus, you should also learn about these 3 warning signs we've spotted with UTS Marketing Solutions Holdings (including 2 which are concerning).

Of course, you might also be able to find a better stock than UTS Marketing Solutions Holdings. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.